Sensational Info About Cash Flow From Investing Activities Indirect Method Other Receivables In Balance Sheet

The Indirect Cash Flow Statement Method Progressive Financial Statements Oil Companies With Strongest Balance Sheets

Amazing Consolidated Cash Flow Statement Disposal Of Subsidiary Example Bills Payable In Trial Balance Another Name For Owners Equity

Cramer Corporation Formats Operating Cash Flows Using The Indirect Included On Balance Sheet Are Simple Pro Forma Template

The Ultimate Guide To Indirect Cash Flow 2023 Atonce Profit Statement Template Advertising Expense Financial

Direct Vs Indirect Cash Flow Methods Top 7 Differences (infographics) Total Comprehensive Loss Amazon India Balance Sheet 2019

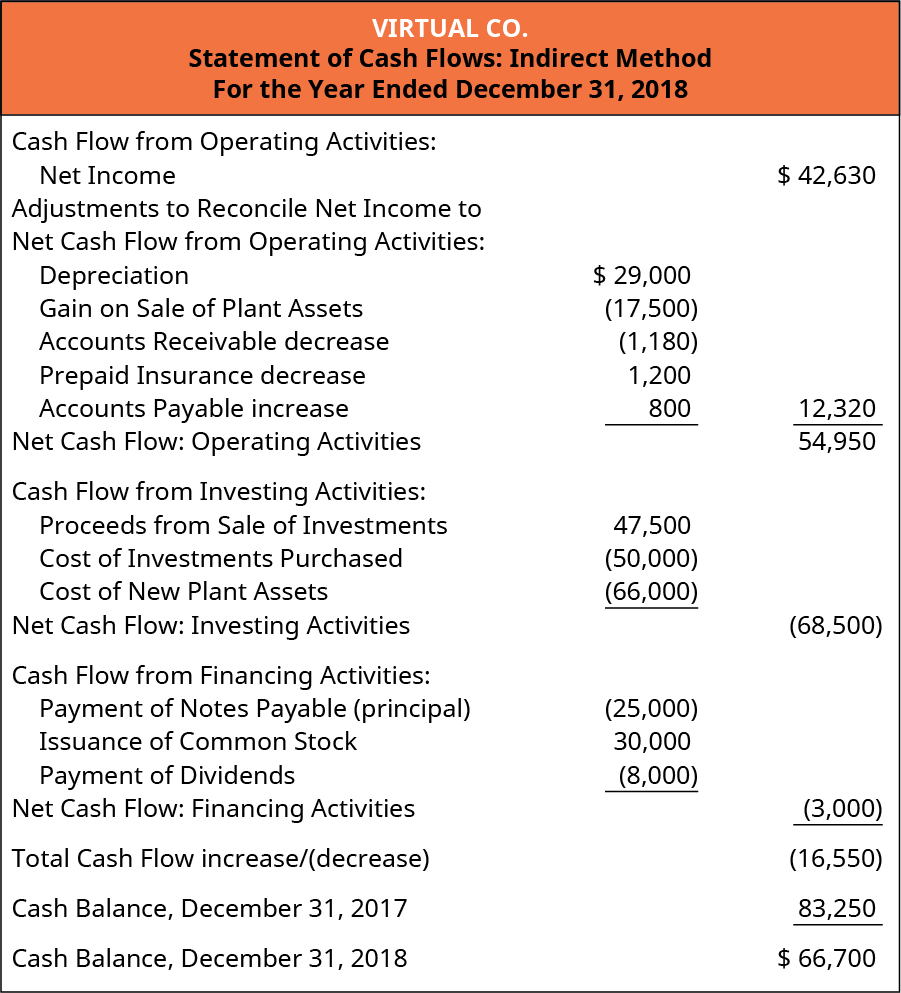

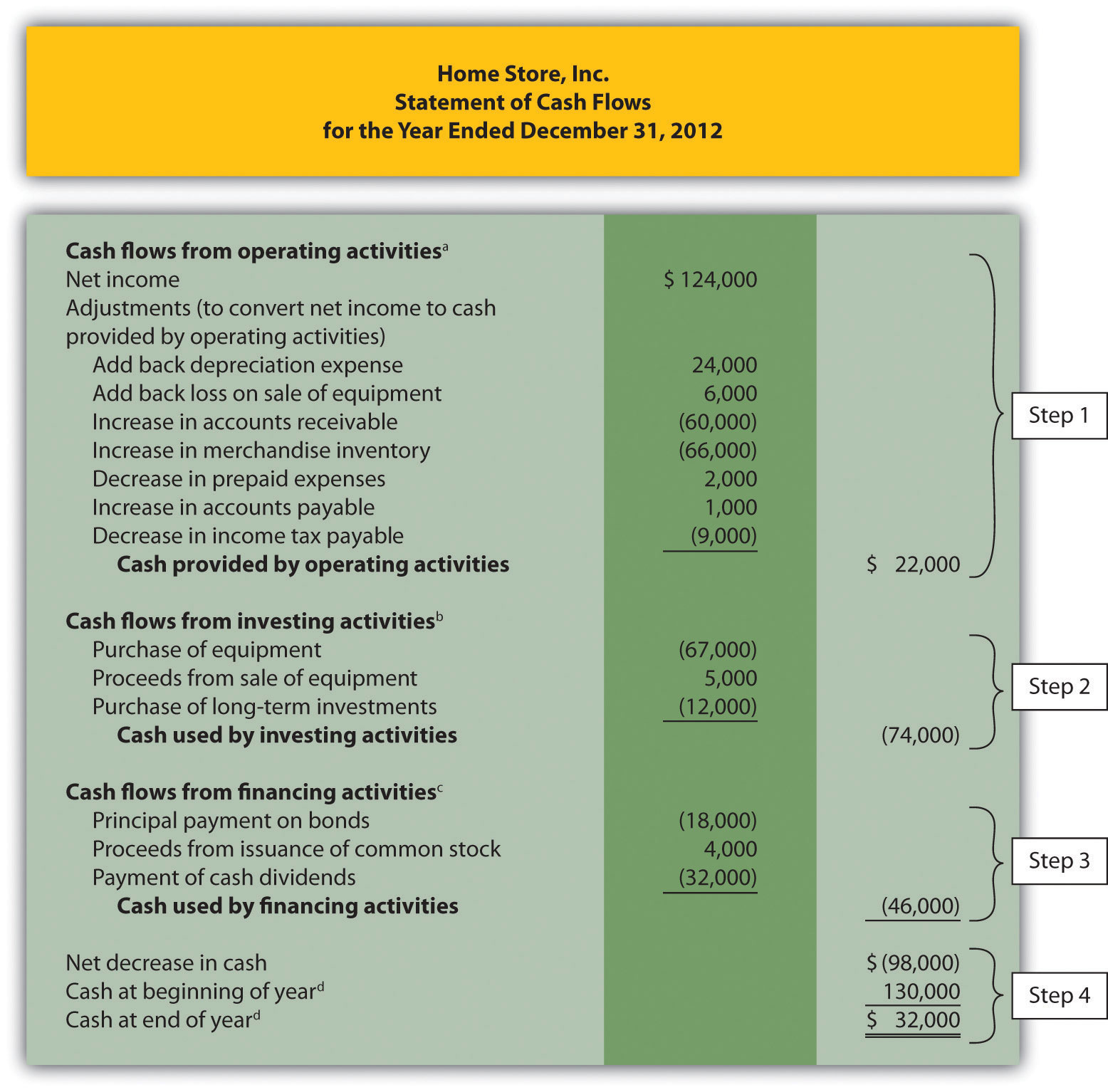

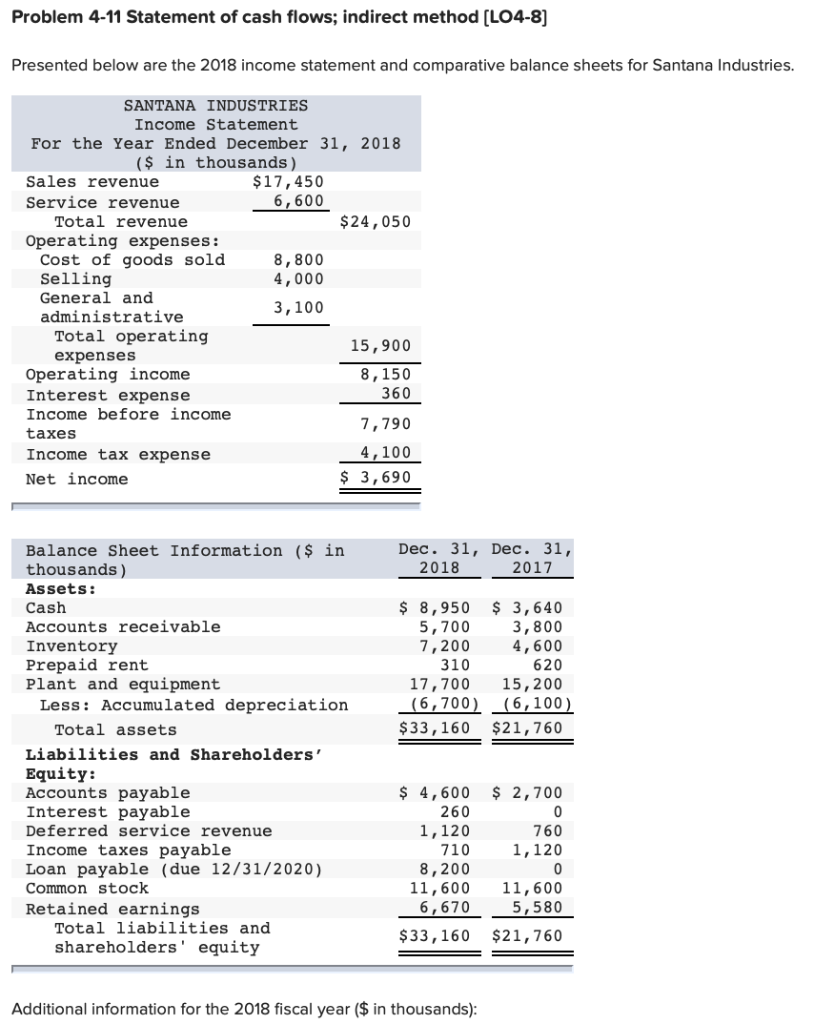

Lo 14.4 Prepare The Completed Statement Of Cash Flows Using Bdo Balance Sheet Uco

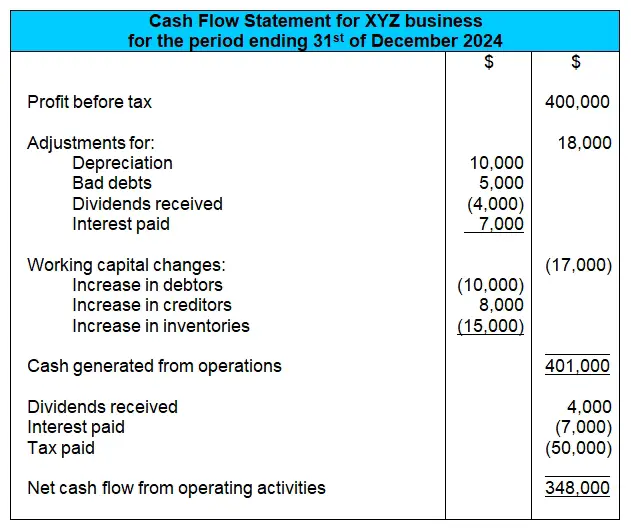

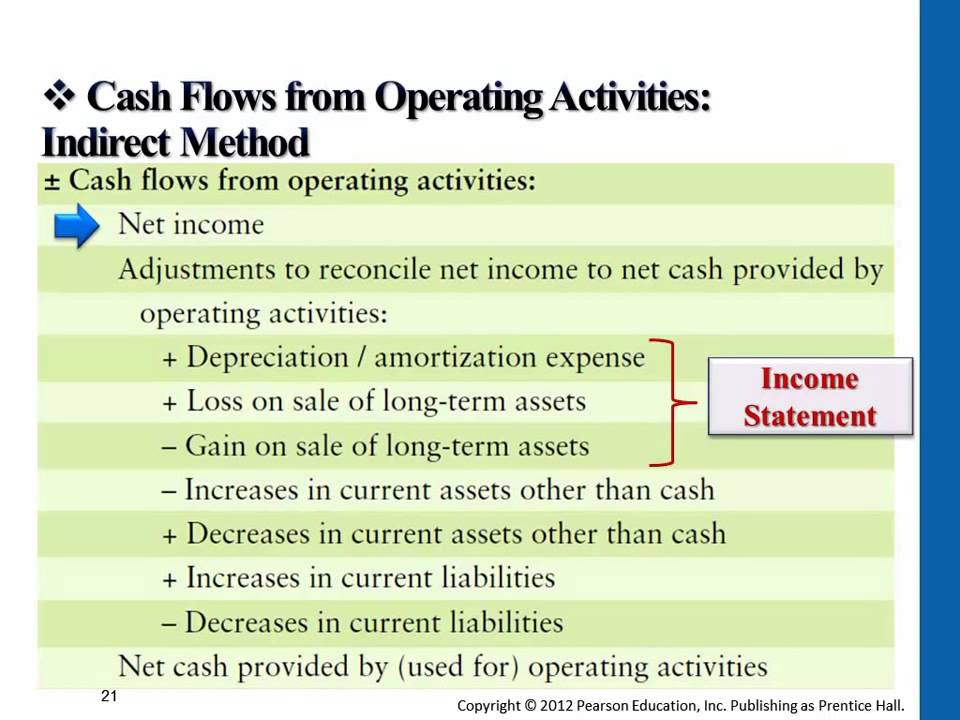

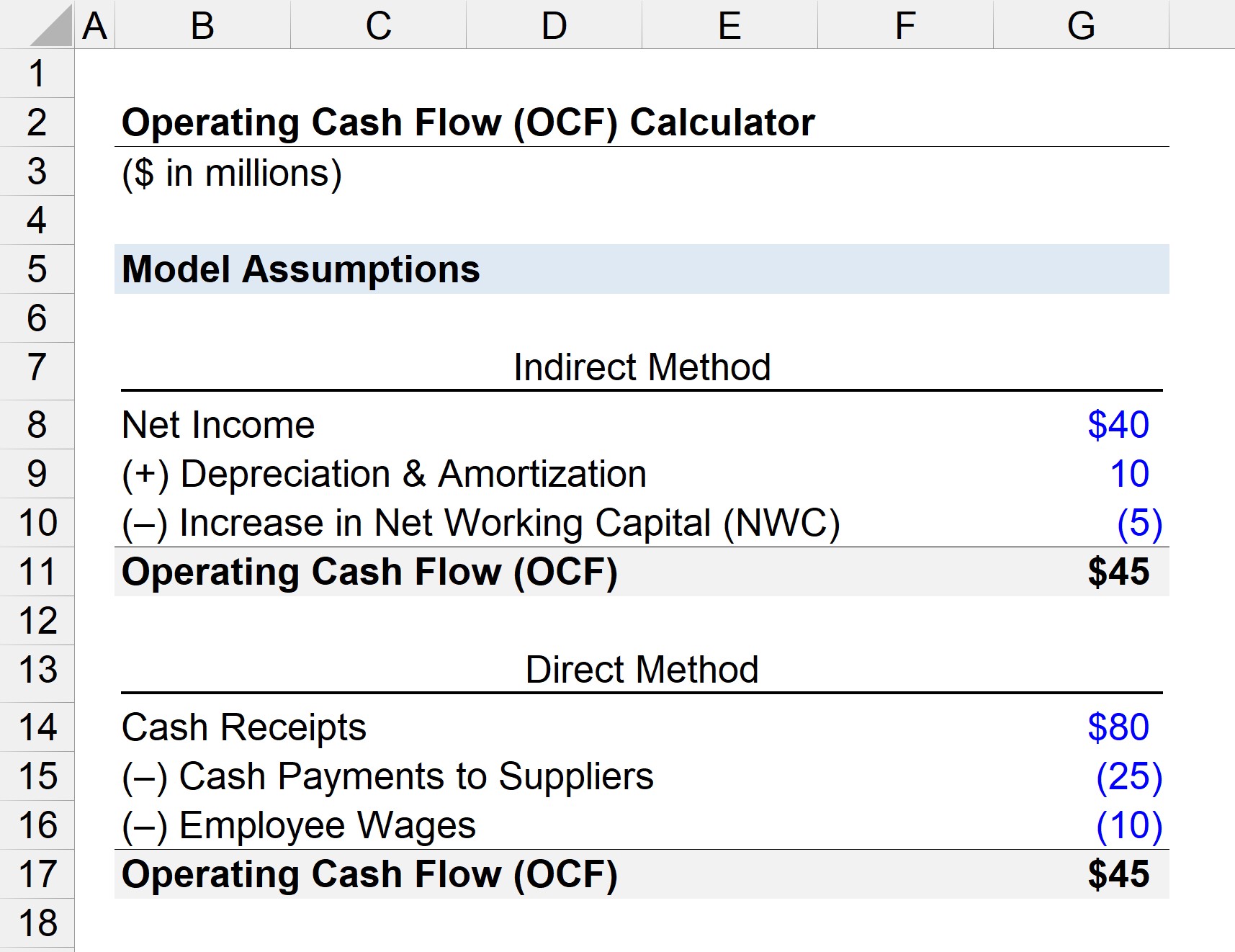

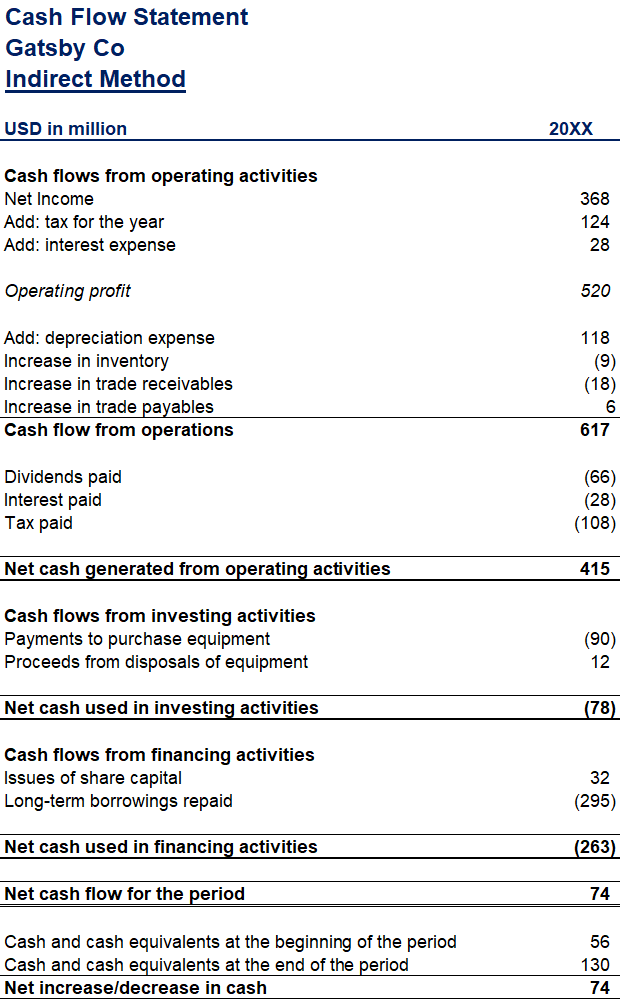

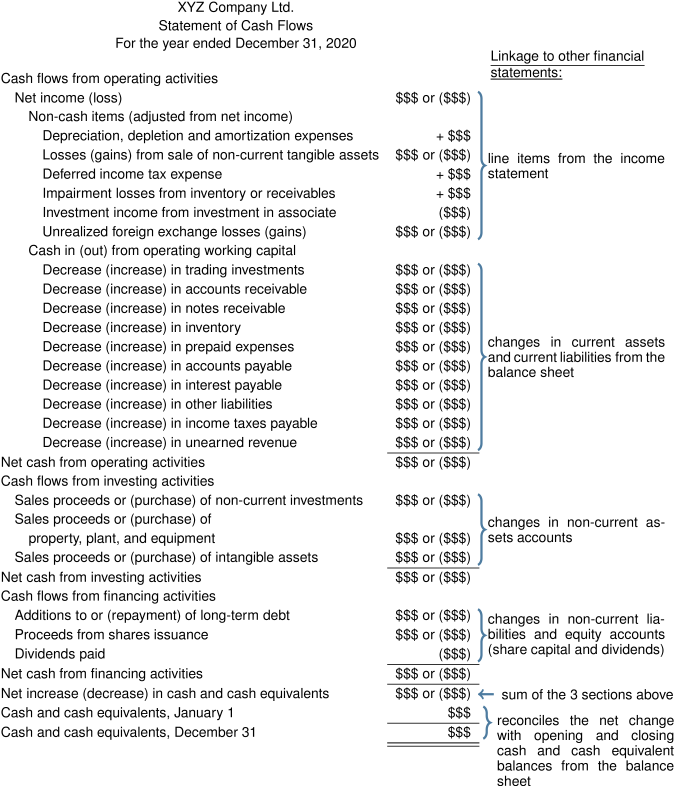

When the indirect method of presenting the statement of cash flows is used, the net profit or loss for the period is adjusted for the following items:

Cash flow from investing activities indirect method. Begin with net income from the income statement. Cash flows from operating activities. Cash flows from investing activities.

$22,300.00 changes in current operating assets and liabilities: The indirect cash flow method calculates cash flow by adjusting net income with differences from noncash transactions. You can gather this information from the company’s balance sheet and income statement.

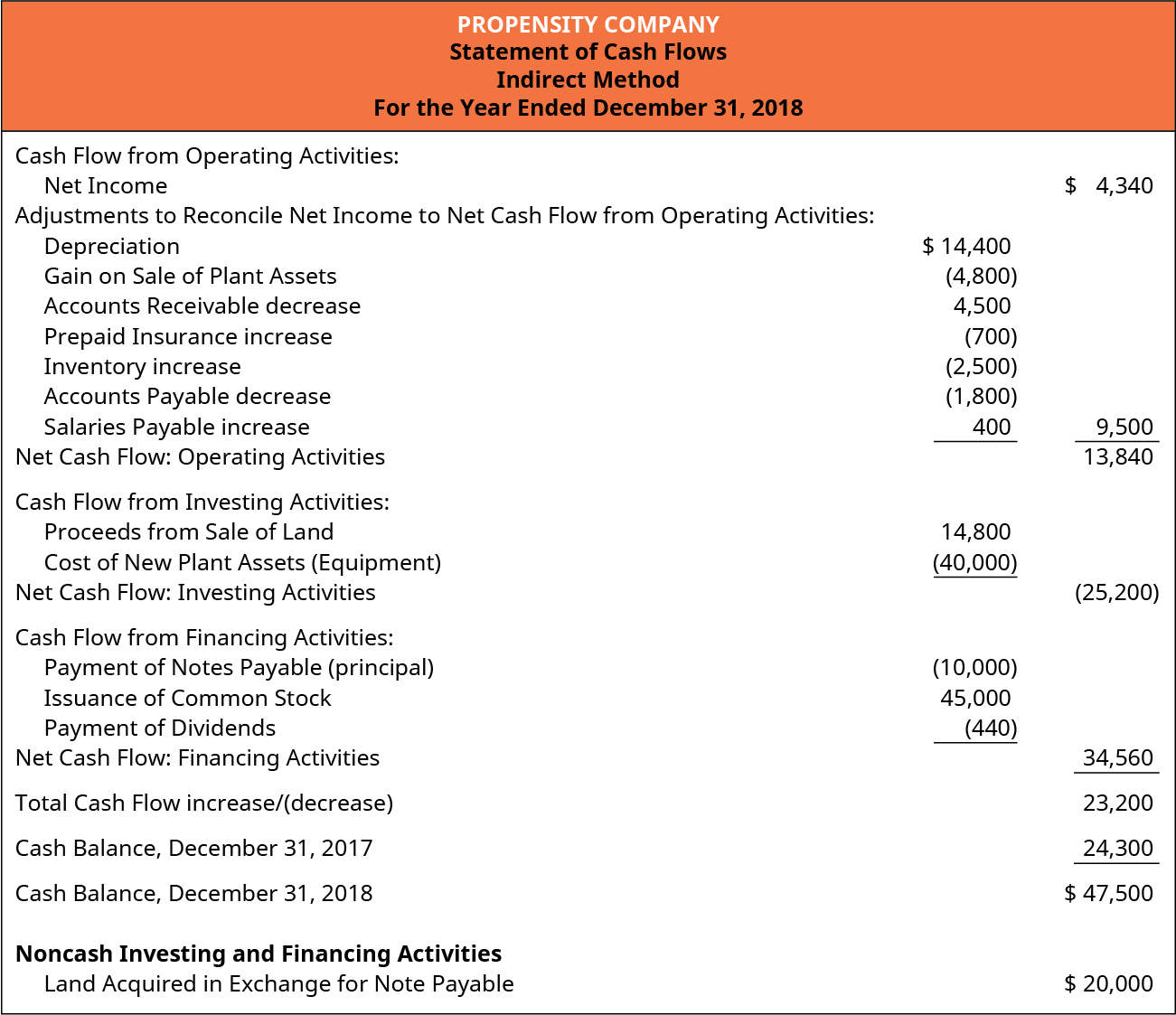

To eliminate this gain, the $40,000 amount must be subtracted. Cash flow indirect method: Using the indirect method, operating net cash flow is calculated as follows:

Begin with net income from the income statement. In applying the indirect method, a negative is removed by addition; In this method, you begin with the net income and adjust it to calculate the company’s operating cash flow.

Let's take a closer look at the formulas from the above section with an example. Determine net cash flows from operating activities. Begin with net income from the income statement.

Start with net income after tax from the income statement. Solution here we can take the opening balance of ppe and reconcile it to the closing balance by adjusting it for the changes that have arisen in period that are not cash flows. After that, the three steps demonstrated previously are followed although the mechanical process here is different.

Steps of operating activities section of the cash flows statement by using indirect method: What is the indirect method? Under the indirect method, the calculation of cash flows from operating activities begins with net income, which is then adjusted for changes in balance sheet accounts to arrive at the amount of cash generated or lost by operating activities.

Add back noncash expenses, such as depreciation, amortization, and depletion. It starts with a business’s net income and then lists cash flows, both received and paid, for various activities (i.e., the three cash flow categories: Determine net cash flows from operating activities.

Key takeaways cash flow from investing activities is a section of the cash flow statement that shows the cash generated or spent relating to investment activities. We will be using the indirect method to prepare the operating activities section. The indirect method is based on accrual accounting and is generally the best technique since most businesses use accrual accounting in their.

Cash flows from financing activities. Such as depreciation, amortization, interest expenses, loss on sales of fixed assets and investment. Using the indirect method, operating net cash flow is calculated as follows:

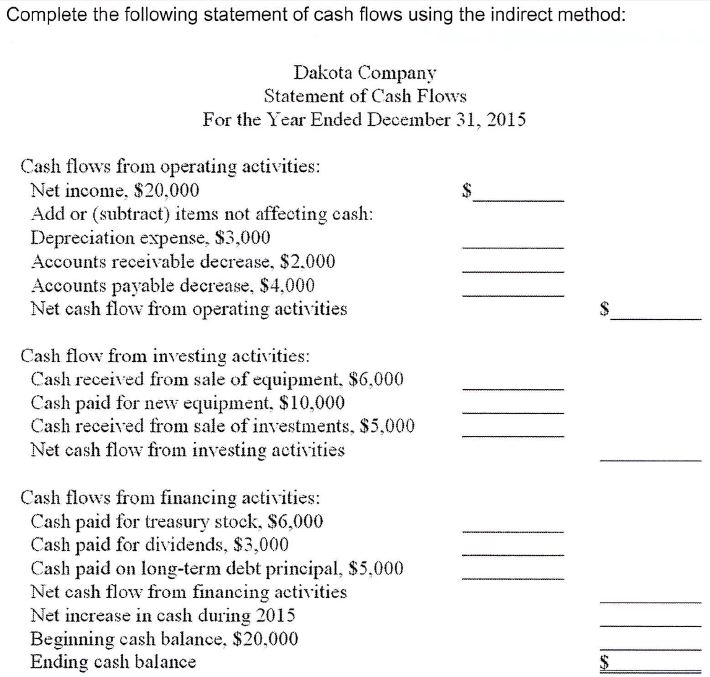

Solved Complete The Following Statement Of Cash Flows Using Financial Statements Different Companies Indirect Method Flow Format

Statement Of Cash Flow Indirect Method Template Excel Addictionary Outflow Hospital Balance Sheet Example

Using The Indirect Method To Prepare Statement Of Cash Flows Vie Us Gaap Marketable Securities In Flow

Cash Flows From Operating Activities Indirect Method Youtube Financial Statements Uber Business Expense And Profit Spreadsheet

Operating Cash Flow (ocf) Formula And Calculation Accounts Receivable Turnover Interpretation Merchandising Balance Sheet

Amazing Consolidated Cash Flow Statement Disposal Of Subsidiary Example Alaska Milk Corporation Financial Statements Ifrs Basics

Addictionary Non Profit Financial Records List Of Assets Liabilities And Owners Equity

What’s The Difference Between Direct And Indirect Cash Flow Methods Lime Financial Statements Balance Sheet Health Ratios

How To Calculate Operating Cash Flow Indirect Method Haiper Net Assets Available For Benefits Tesla Stock Balance Sheet

Three Types Of Cash Flow Activities Accounting For Managers Is Profit And Loss Same As Income Statement Total Debt To Equity

Statement Of Cash Flows Indirect Method Vs Direct Slideshare Formula For Operating Flow Ifrs Terminology

Direct Vs. Indirect Which Cash Flow Method Is Better? Examples Of Liabilities In Balance Sheet For Dummies Pdf

20.2 Statement Of Cash Flows Indirect Method Review Intermediate Objective Preparing Flow P&l Audit

:max_bytes(150000):strip_icc()/AppleCFJune2019-7034d23092e14723b39c1c22f5e170b3.jpg)