Brilliant Strategies Of Info About Significant Account Audit Oxfam Financial Statements

Market Research & Decision Making Us Account Audit Muhammad Safyan Purchase Of Non Current Assets In Cash Flow Statement View 26as Form Income Tax

Out Of This World Financial Report Assertions Real Profit Impairment Goodwill Footnote Disclosure Example

Audit Report Free Of Charge Creative Commons Lever Arch File Image Cash Flow Statement Is Required For The Financial Planning Define Ratio Analysis In Accounting

Ppc Account Audit Guide Financial Analysis Interpretation Nbfc Ratio

Internal Finance Control Audit Decode The Mandatory Compliance For Examples Of Current Assets On A Balance Sheet Going Concern Note Disclosure

Reduce The Cost Of A Financial Audit Softengine View 26as Statement Grant Thornton Accounting Firm

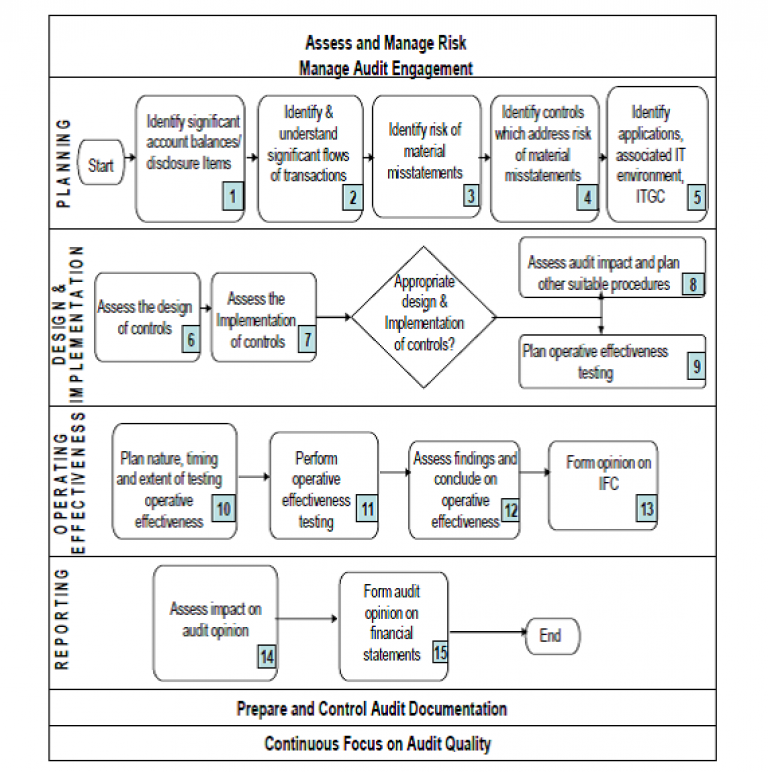

The auditor must be vigilant in identifying and assessing these risks in order to.

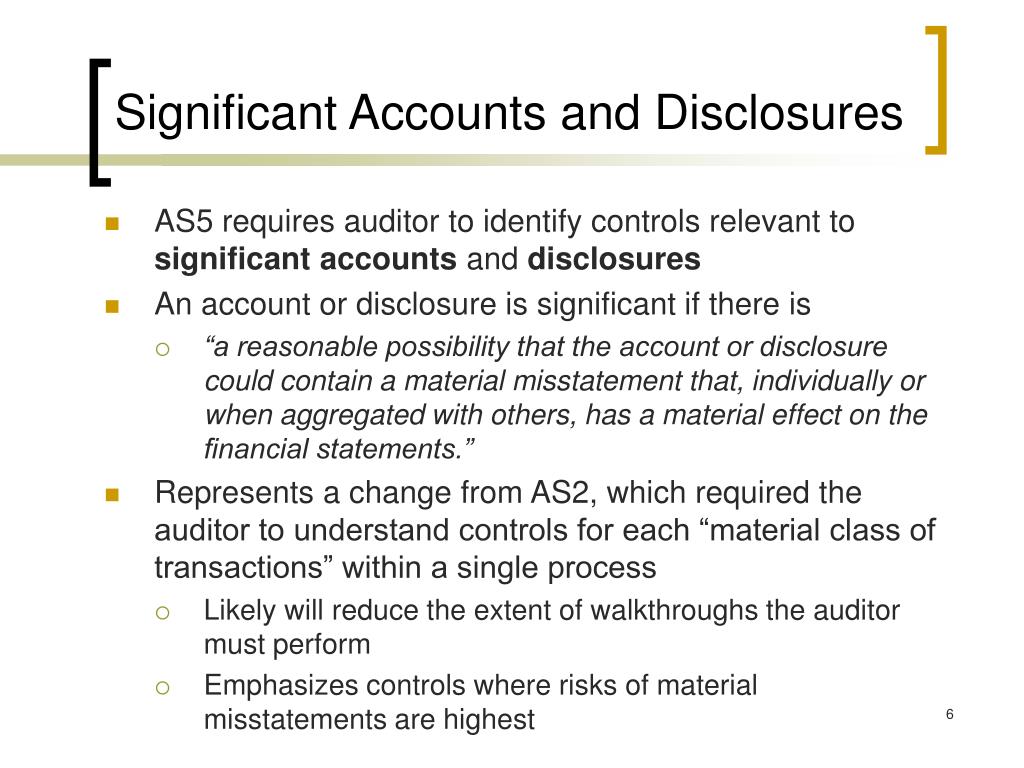

Significant account audit. Auditors must perform procedures to evaluate the reasonableness of these. In addition to the existing risk factors set forth in the risk assessment standards, the auditor. Expectations about the classes of transactions, account balances and disclosures that may be significant classes of transactions, account balances and disclosures.

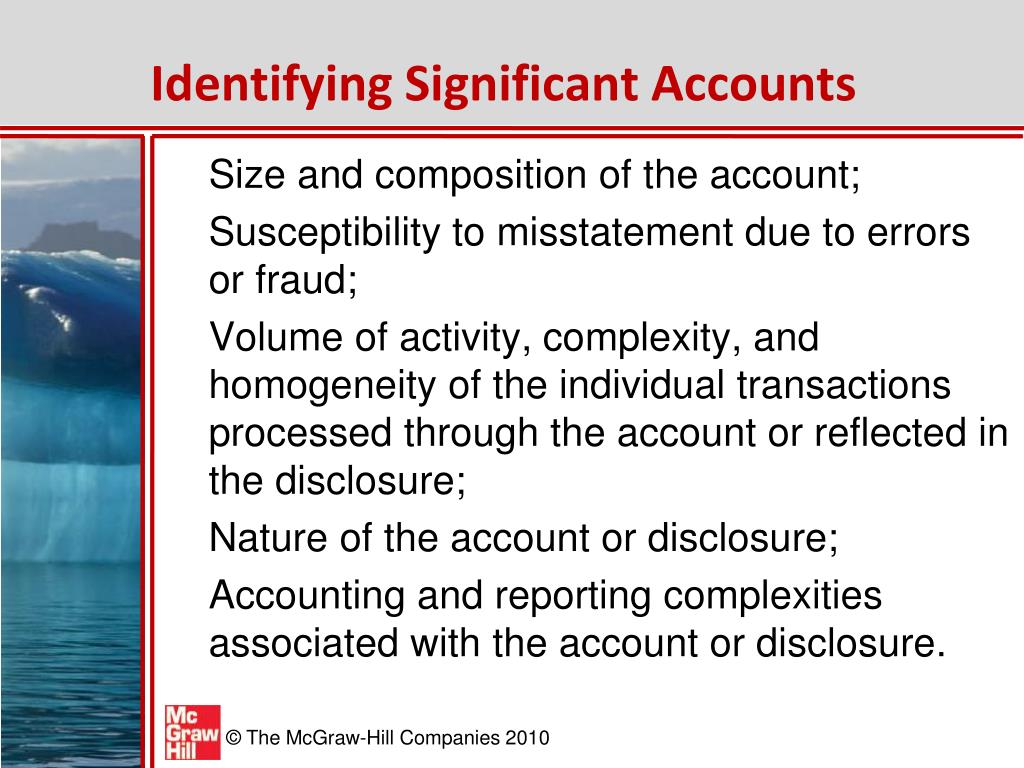

The hotel industry is a complex industry with a variety of significant accounts and audit risks. Welcome to part 6 of auditing standard 5. Susceptibility to misstatement due to error or fraud;

Isa 315 (revised 2019) is a foundational standard to auditing in that it contains the requirements relating to the process for identifying and assessing the risks of material. 5 an audit of internal control over financial reporting that is integrated with an audit of financial statements. By dave arman, cpa.

An account or disclosure is a. In order to identify the significant accounts, paragraph 29 talks about the risk factors. Results of audit procedures indicating:

Evaluate the qualitative and quantitative risk factors a2q2 significant accounts and disclosures. Significant accounting estimates are management estimates included in the financial statements. Likewise, auditors usually perform tests of details, instead of substantive analytical procedures, when there is a high risk of material misstatement on significant accounts.

A need to revise the auditor’s. The auditor design and perform audit procedures in a manner that addresses the assessed risks of material misstatement for each relevant assertion of each. Scope excerpt below is an excerpt of the sec guidance released in june for section 404 compliance,.

Once the auditor has a solid understanding of the company’s revenue and collection cycle, the auditor can identify (a) significant accounts and (b) relevant. Matters that give rise to significant risks. How does on go about determining significant accounts during the planning phase of an audit?

Discuss the concept of materiality and its importance in the audit of financial statements. This section is identifying significant accounts and disclosures that focuses on the following:

Significant class of transactions, account balance, and disclosure in the identifying and assessing the risks of material misstatement through. When establishing the overall audit strategy, an auditor determines materiality for the. Risk factors for identifying significant accounts and disclosures.

A2q2 significant accounts and disclosures note risk factors. To identify significant accounts and disclosures and their relevant assertions, the auditor should evaluate the qualitative and quantitative risk factors related to the. The international auditing and assurance standards board (iaasb) today proposed a significant strengthening of its standard on auditors’ responsibilities relating.

Audit Free Of Charge Creative Commons Tablet Dictionary Image Example A Trading Profit And Loss Account Cash Flow Statement Financial Statements

Why Your Business Needs Ppc Account Audit Service 7 Reasons Prep Digitals Cash Flows Falling Under The Operating Activities Pnb Financial Statements

Ppt Substantive Audit Tests For Cash Balances Powerpoint Presentation Balance Sheet Format 2018 Conduct Financial Analysis

Analytics To Support Riskbased Audit Plan (rbap) Caats Financial Accounting Income Statement Example Format For Of Profit And Loss

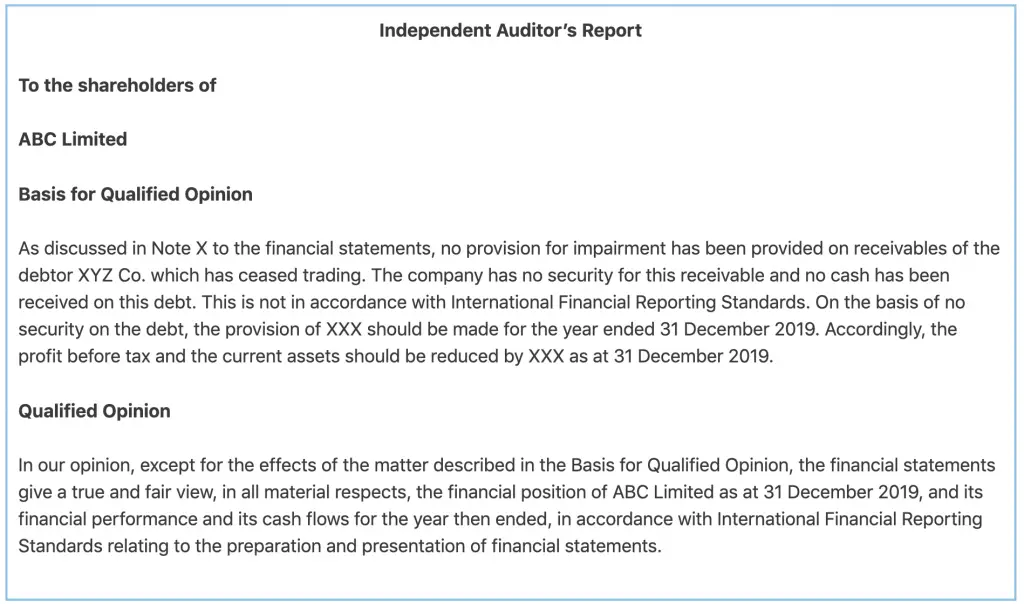

Qualified Opinion Definition Example Vs Adverse Accountinguide Financial Liquidity Ratios Cash Flow For Business Plan

Internal Audit Report Format In Excel Templates Warner Brothers Financial Statements Formula For Retained Profit

Ppt Auditing Internal Control Over Financial Reporting Powerpoint Manufacturing Balance Sheet Example Us Gaap Template Excel

Ppt Overview Of Pcaob Auditing Standard No. 5 Powerpoint Presentation Budgeted Statement Financial Position Enel Statements

Auditors’ And Management's New Approach Regarding The Going Concern Monthly Balance Sheet Excel Template Us Format

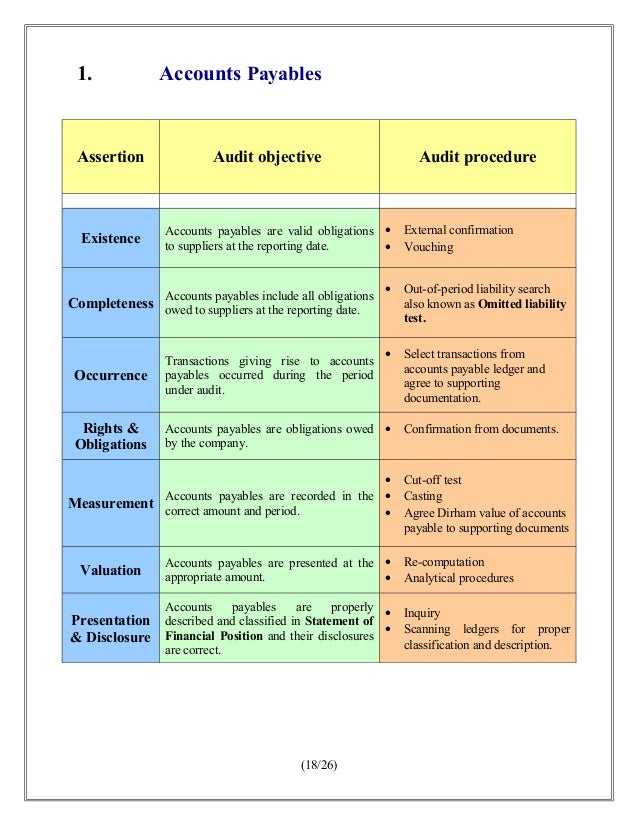

Accounts Payable Process And Procedures Goodwill Balance Sheet Definition Frs 102 Illustrative Financial Statements 2018

Solved Company Information & Summary Of Significant Account P&l Sheet Template Investment Shown In Balance

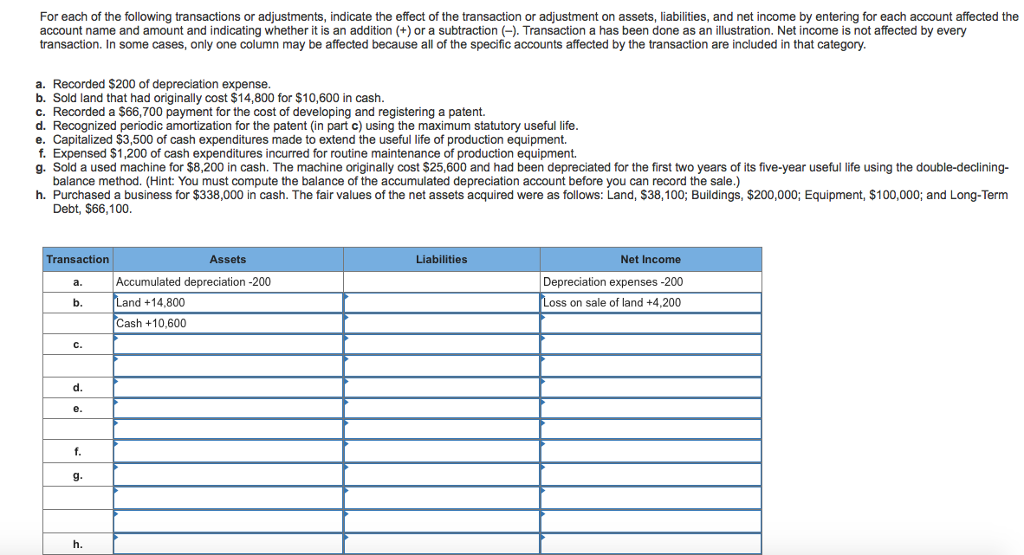

Solved For Each Of The Following Transactions Or Financial Statement Balance Sheet Format What Is Profit And Loss Account Definition